“In the UK construction sector, failing to grasp CIS payroll could cost you up to 20% in unexpected tax deductions, turning a profitable project into a financial headache,” warns tax expert Sarah Jenkins from the Chartered Institute of Taxation.

Key Areas We Will Cover

- What CIS payroll entails and why it matters for construction businesses

- The difference between gross and net payment status under CIS

- Step-by-step guide to registering for CIS payroll

- How CIS deductions work in practice, including rates and calculations

- Benefits and compliance tips for smooth payroll management

- Common pitfalls and how to avoid them

Introduction

CIS payroll forms the backbone of tax compliance in the UK’s construction industry, ensuring that subcontractors receive payments while HM Revenue and Customs (HMRC) collects income tax and National Insurance contributions at source. For contractors and subcontractors alike, mastering CIS payroll is essential to avoid penalties, maintain cash flow, and build sustainable operations. This guide, updated as of October 2025, explores everything from basics to advanced strategies, incorporating recent HMRC developments such as expanded scope for traffic management services and preparations for Making Tax Digital (MTD). It equips you to navigate the scheme with confidence and optimise your financial processes.

What is CIS Payroll?

The Basics of the Construction Industry Scheme

The Construction Industry Scheme (CIS) is a government programme introduced in 2000 to tackle tax evasion in construction by deducting taxes directly from subcontractor payments. CIS payroll specifically refers to the process where contractors act as ‘deemed employers’, withholding 20% (or 30% for unregistered parties) from payments before disbursing the net amount.

Under CIS, a contractor is defined as a business or other concern that pays subcontractors for construction work. This includes construction companies, building firms, government departments, local authorities, and other businesses typically known as ‘clients’. A subcontractor is a business that carries out construction work for a contractor. Notably, where a worker is supplied to a contractor by or through an agency and the worker performs construction operations under a contract with the agency, the agency is considered the subcontractor, and the contractor must apply CIS rules to payments made to the agency. However, if the agency merely introduces the worker and the worker contracts directly with the contractor, the agency is not the subcontractor.

This system streamlines tax collection but requires meticulous record-keeping. Unlike standard PAYE payroll, CIS focuses solely on construction-related payments, excluding materials unless bundled with labour.

Construction work under CIS encompasses various activities related to permanent or temporary structures, such as:

- Civil engineering works, including rail and maritime.

- Demolition.

- Building, alterations, and repairs.

- Decorating.

- Site preparation, such as providing access works.

- Installations of systems, including power, lighting, and heating.

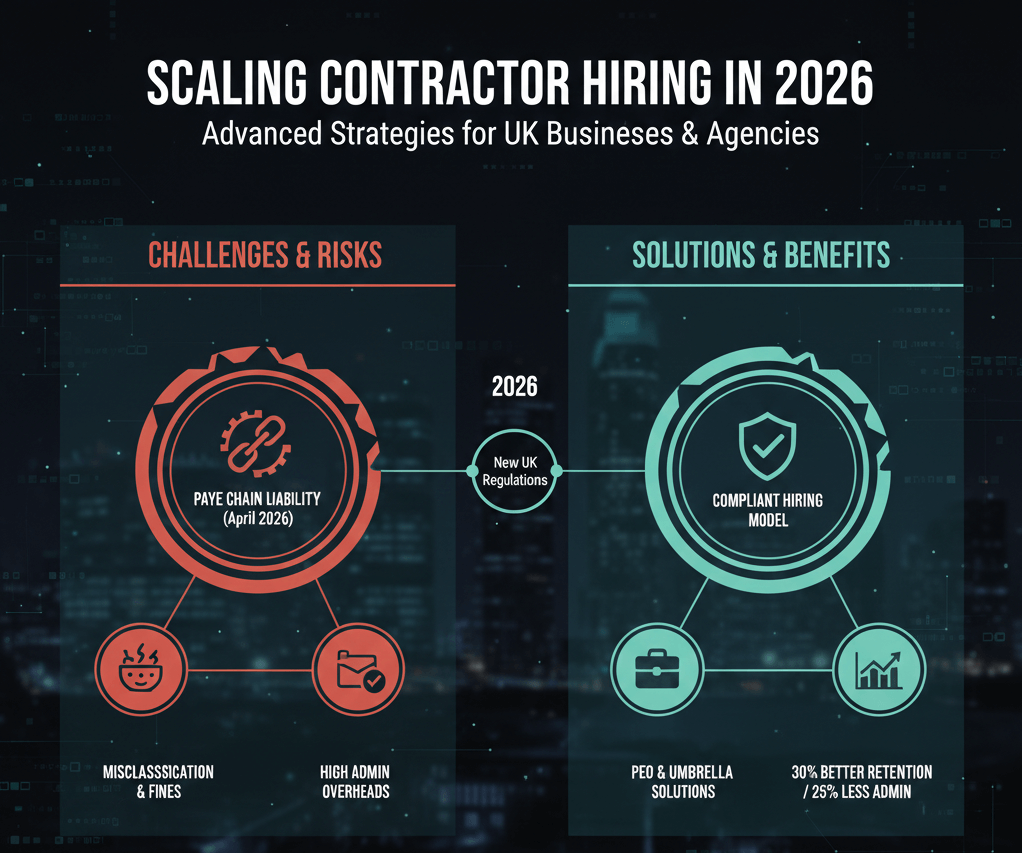

Recent developments effective from March 2025 have expanded CIS scope to include certain traffic management services (e.g., road traffic control and signage) in specific circumstances, requiring affected businesses to register and apply deductions accordingly. Looking ahead, from April 2026, Making Tax Digital (MTD) for Income Tax Self-Assessment will mandate digital record-keeping for most self-employed CIS workers (including sole traders and partnerships with income over £50,000), necessitating compatible software for compliance.

Why CIS Payroll is Crucial for Your Business

Effective CIS payroll management safeguards against HMRC audits, which have surged by 15% in recent years according to official statistics. It also fosters trust between contractors and subcontractors, ensuring timely verifications and reducing disputes over deductions. Non-construction businesses may also qualify as ‘deemed contractors’ if their construction expenditure exceeds £3 million over 12 months, triggering mandatory registration.

Gross vs Net Status in CIS Payroll

Understanding Gross Payment Status

Gross status allows subcontractors to receive full payments without deductions, provided they meet strict criteria, including a turnover threshold (net of VAT and materials) of at least £30,000 for sole traders; £30,000 per partner or £100,000 for the entire partnership; and £30,000 per director or £100,000 for the company over the last 12 months. Additional requirements include timely payment of tax and National Insurance, engagement in UK construction work, and operation of a UK-based business with a compliant bank account. Achieving gross status demands robust bookkeeping, making it ideal for established firms with strong compliance records.

- Eligibility Check: Submit form CIS300 to HMRC for assessment.

- Advantages: Better cash flow and competitive bidding power.

Net Payment Status Explained

Net status triggers standard deductions of 20% from labour payments, rising to 30% if unverifiable. It is the default for new entrants and suits smaller operations still building credentials.

- Transition Tips: Use verified Unique Taxpayer Reference (UTR) numbers to lower rates quickly.

- Drawbacks: Impacts liquidity, so plan finances accordingly.

Choosing the Right Status for Your Payroll Needs

Switching statuses requires HMRC approval, but regular reviews can unlock gross benefits. Tools like payroll software integrate CIS calculations seamlessly, minimising errors.

For quick reference:

|

Aspect |

Gross Status |

Net Status |

|

Deductions |

None (full payment) |

20% (registered) or 30% (unregistered) |

|

Eligibility |

Meets turnover thresholds (£30,000+), compliance history |

Default for new/smaller operations |

|

Advantages |

Improved cash flow, self-managed taxes |

Simpler entry, but reduced liquidity |

|

Application |

Via HMRC form CIS300 or online |

Automatic upon registration |

How to Register for CIS Payroll

Step-by-Step Registration Process

Registering as a contractor is straightforward via HMRC’s online portal, taking just 15 minutes. Gather essential details, including:

- Your company’s Corporation Tax number (also known as UTR) from form CT416.

- Directors’ National Insurance (NI) numbers and dates of birth.

- Company Registration number, VAT number, and contact details.

- PAYE reference number and Accounts Office Reference Number.

- Gross turnover figure and cost of materials purchased.

- Company bank details.

- Directors’ personal UTR numbers.

Complete the CIS registration form, declaring subcontractor payment intentions, and receive your CIS number within five working days. Subcontractors must register separately to obtain verification, essential for reducing deduction rates.

Ongoing Verification and Monthly Returns

Post-registration, verify subcontractors monthly using HMRC’s helpline (0300 200 3210) or Gross Payment Status service. File full payment statements (FPS) via compatible payroll software, detailing deductions for each period. Monthly returns are required even for nil payments, due by the 19th of the following month.

Calculating and Handling CIS Deductions

Deduction Rates and Thresholds

Standard labour deductions stand at 20%, applied after excluding VAT and materials. For example, on a £10,000 invoice (80% labour), deduct £1,600, paying £8,400 net.

- 30% Rate Scenario: Applies to unverified parties.

- Zero Rate: Rare who has gross status, granted only to those paying other sub-contractors.

Practical Payroll Integration

Incorporate CIS into your payroll cycle by:

- Issuing payment and deduction statements promptly.

- Reclaiming deductions via your annual tax return.

- Using automated tools to track cumulative payments against £50,000 annual thresholds for nil returns.

Benefits of Optimised CIS Payroll Management

Financial and Operational Gains

Streamlined CIS payroll boosts cash flow by 10-15% through accurate gross claims and reduces admin time by half with digital solutions. It also enhances subcontractor retention, critical in a sector facing 20% labour shortages.

Compliance and Risk Reduction

Proactive management averts £3,000 average fines per breach. Regular audits and training ensure adherence, positioning your business as a reliable partner. For MTD readiness from April 2026, invest in HMRC-compatible software to maintain seamless compliance.

Common CIS Payroll Mistakes and How to Avoid Them

Pitfalls to Watch For

Overlooking material exclusions or failing to verify statuses tops the list, leading to over-deductions and disputes.

- Error Example: Deducting from full invoices instead of labour portions.

- Solution: Implement dual-check systems in payroll software.

Expert Strategies for Success

Partner with CIS specialists for audits, and leverage HMRC’s free webinars (available at gov.uk). Stay updated via Constructionline for scheme changes, ensuring your processes evolve. For deemed contractors, monitor expenditure thresholds to avoid unexpected registration obligations.

Conclusion

CIS payroll, while complex, empowers construction professionals to comply efficiently and thrive financially. From grasping gross versus net statuses to mastering deductions, the key lies in proactive registration, accurate calculations, and ongoing vigilance now including adaptations for 2025 expansions and 2026 MTD requirements. By prioritising these elements, you not only mitigate risks but also unlock growth opportunities in a competitive landscape. Always consult HMRC or a qualified tax advisor for personalised guidance.

Frequently Asked Questions About CIS Payroll

Navigating CIS payroll raises common queries for many in the construction sector. Below, we address the most pressing ones to clarify uncertainties and support informed decision-making.

CIS payroll targets construction payments with source deductions, whereas PAYE applies broader employee withholdings including pensions.

Monthly full payment submissions are due by the 19th of the following month, with nil returns if no payments occur.

Yes, via your Self Assessment tax return, offsetting against income tax liabilities.

HMRC may recover shortfalls from you, plus interest and penalties up to 100% of the underpayment.

Not required, but highly recommended for accuracy and HMRC compatibility, reducing error risks significantly especially for MTD compliance from April 2026.

If an agency supplies a worker who contracts directly with the agency for construction work, the agency is the subcontractor, and CIS deductions apply to payments from the contractor to the agency. If the agency only introduces the worker, it is not involved in CIS.

Nil returns must still be filed by the 19th of the following month to maintain compliance.

Ready to Streamline Your CIS Payroll? Take Action Today

Contact FutureLink Group for a free CIS compliance audit and tailored payroll solutions. Visit our CIS services page, email us at sales@futurelinkgroup.co.uk or call +44 (0) 1923 277900 to get started, ensuring your construction business operates smoothly and profitably.

Craig Moss

Craig Moss is a seasoned professional in the employment and recruitment industries, based in Kings Langley, UK. With over 30 years of experience, including a successful tenure as a central London realtor handling properties up to £3 million, he now leads an exciting management role at Futurelink Group. Specialising in compliant payroll solutions for contract recruitment, Craig helps clients increase margins by up to 30% while navigating complex legislation. His people-focused approach, honed through decades in sales and people management, ensures both recruiters and workers benefit from tax-efficient, compliant solutions. Passionate about building strong relationships, Craig thrives on delivering results that drive business success.