Over the last decade, full-time employment has been declining in favour of freelancers and contract workers. Around 15% of the UK workforce is self-employed and this is an even higher percentage in the construction industry which is estimated to be in the order of 30 to 40%. So how exactly has the impact of IR35 affected the construction industry?

The trend is showing some signs of reversal with large contractors like Laing O’Rourke committing to a permanent workforce. Naturally, it is more common to find self-employed workers with specialist subcontracting companies (roofers, scaffolders, ground workers etc.) versus project management firms like Laing O’Rourke, Mace and Bovis, for example.

A common approach by contract workers has been to set up a limited company, or PSC (personal service company). PSCs are still one of the most tax-efficient ways to contract and there are estimated to be more than 250,000 PSCs in the UK, many working in construction.

Introduction of IR35 Regulations

So that all sounds great but HMRC decided to ruin the party back in 1999 with the introduction of IR35, an anti-avoidance tax legislation designed to tax “disguised employment”. The legislation imposed a series of tests to verify whether the relationship should actually be classified as being self-employed or if it was in effect an employee relationship.

The original legislation required the Ltd Company contractor to assess whether they are inside or outside of IR35, and unsurprisingly as it is in their interest to seek the tax benefits, many PSCs have deemed themselves to be outside of IR35.

Revision to IR35 Legislation

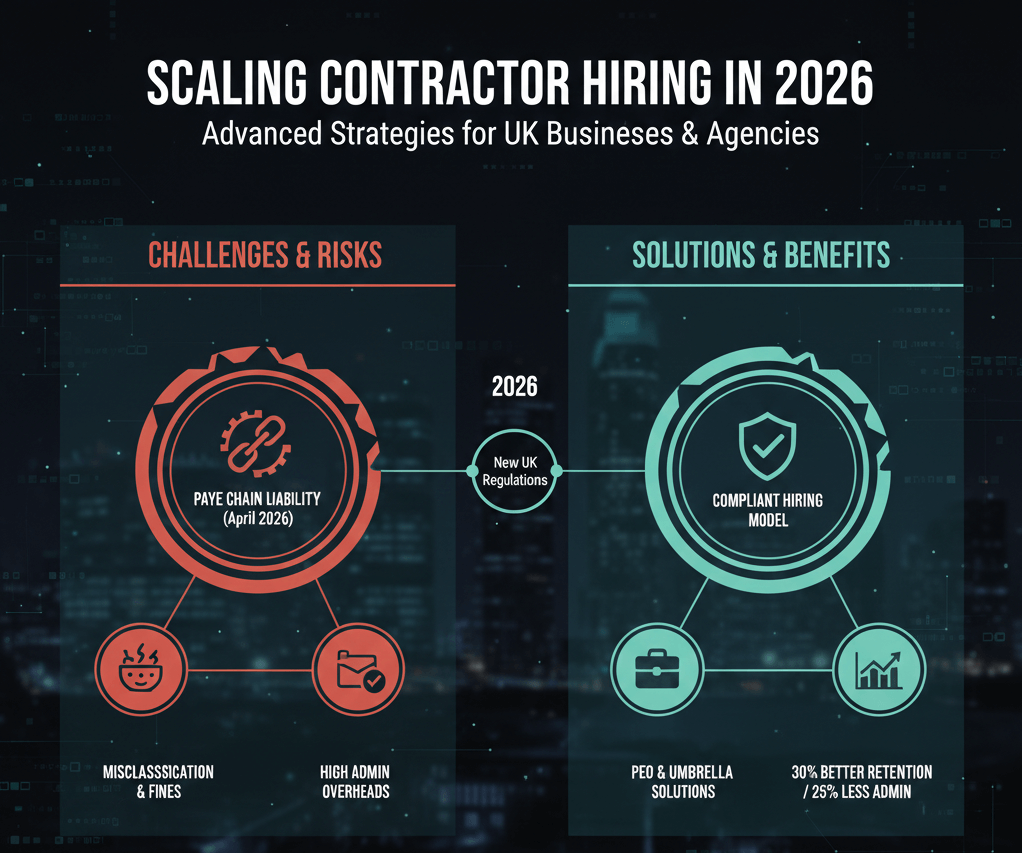

With the introduction of the Onshore Intermediary Legislation in 2014, construction firms and other businesses would now need to assess their self-employed workforce and evaluate the risks they face before IR35 comes into force 6th April 2021. A self-policing policy was imposed by HMRC insisting that all parties in the employment food chain (client company, intermediary company and/or recruitment agency) were asked to check if the worker was supervised – hence the SDC test – asking to assess if the worker was supervised, directed and/or controlled in some way. The legislation has affected those contract workers who have their own limited company, as well as sole traders (CIS) where 20% tax is traditionally deducted at source.

Whether it be the client company, payroll provider or agency intermediary, one would now be responsible for producing and submitting a quarterly report, the first of which was due in August 2015. Heavy fines were and continue to be imposed on those who ignore the deadlines and obligations to submit earning reports.

In 2017, the rules changed affecting the Public Sector and the onus to prove self-employed status became the responsibility of the hirer. This has primarily impacted health and social care, government and education jobs. If proven to be inside of IR35, the worker would be treated as an employee and pay tax and National Insurance under PAYE. Worst still, the worker would not receive employee benefits. Getting this wrong and assuming the worker fell outside of IR35 meant that the hirer would face fines. Hiring contract workers is now a minefield and more so, a complicated affair!

What Can We Do To Help?

To ensure your firm and workers are fully compliant with all current forms of legislation, Futurelink Group provides a free health check service. In most cases, we can maintain the workers’ self-employed status and manage all the quarterly reports, thereby removing any potential fines.

For any other query or to find out more about our payment solutions please visit our page on CIS (Construction Industry Scheme). Alternatively, please call us on 01923 277900.