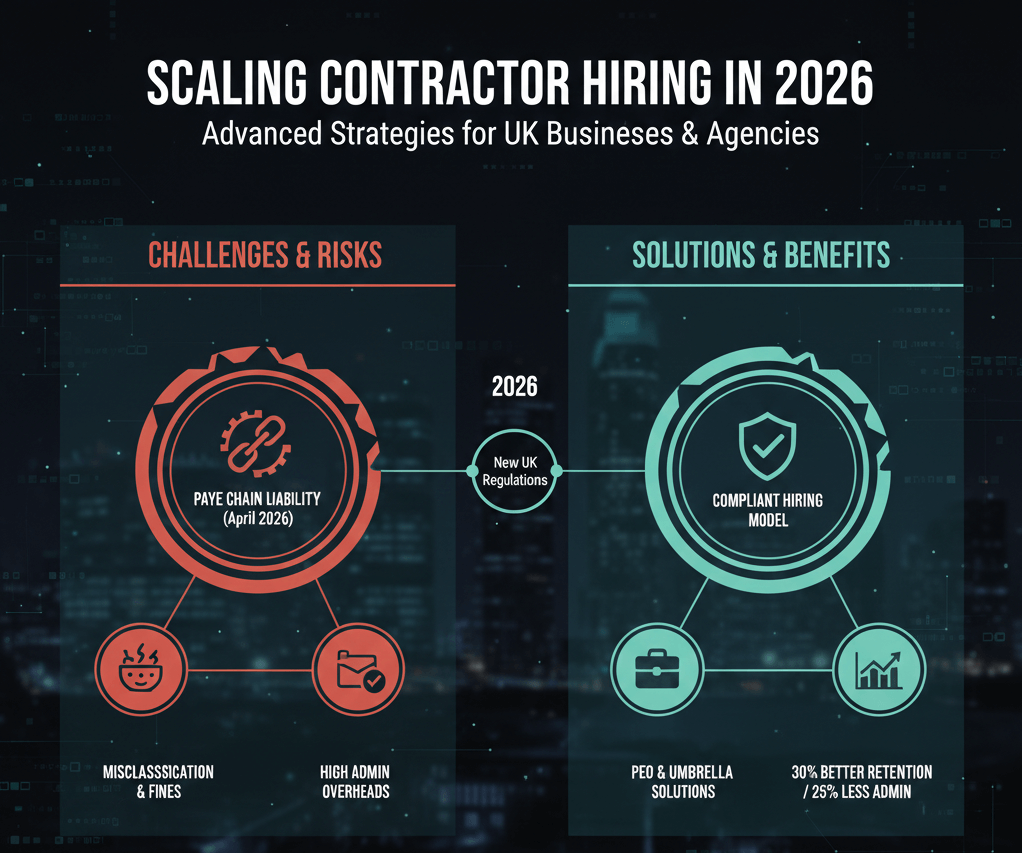

Did you know that from April 2026, new Joint & Several Liability rules will hold agencies and clients accountable for umbrella payroll errors in supply chains, even with international elements? As more UK contractors take on overseas roles in energy, engineering, and construction, staying compliant across borders has never been more critical to avoid unexpected liabilities.

Key Areas We Will Cover:

- UK tax residency rules and how overseas work affects them

- Double Taxation Agreements and avoiding double taxation

- Key 2026 updates, including Joint & Several Liability and Making Tax Digital

- Compliance challenges for contractors in sectors like Oil and Gas, Energy, and Construction

- How Futurelink Group’s solutions ensure seamless tax handling abroad

Introduction:

Tax compliance when working overseas remains a major concern for UK contractors in 2026, particularly amid rising remote and international assignments in high-demand sectors. Navigating UK residency tests, host country obligations, Double Taxation Agreements, and emerging rules like Joint & Several Liability requires careful planning to prevent penalties or overpayments. This updated guide explores current requirements and demonstrates how partnering with a specialist like Futurelink Group simplifies payroll, ensures full compliance, and maximises take-home pay through tailored Sole Trader, umbrella PAYE, PEO, or CIS solutions.

Understanding UK Tax Residency for Contractors Abroad

Your UK tax residency determines much of your liability. Under the Statutory Residence Test, spending fewer than 183 days in the UK per tax year, combined with limited ties, can make you a non-UK resident, taxing only UK-sourced income.

However, short overseas stints (under 183 days) often maintain UK residency, requiring worldwide income reporting via Self Assessment. Hybrid roles or frequent travel complicate this; track days meticulously to avoid surprises.

Double Taxation Agreements: Preventing Double Taxation

The UK has DTAs with over 100 countries to allocate taxing rights and provide relief.

If working abroad exceeds host country thresholds (often 183 days), that country may tax employment income, but DTAs typically allow credits or exemptions in the UK.

Key considerations:

- No permanent establishment created by your activities or employer.

- Claim relief via Self Assessment or employer adjustments.

- For non-residents, recent changes (e.g., removal of notional dividend credits from April 2026) affect certain income.

DTAs protect against double taxation but require proper documentation.

2026 Updates Impacting Overseas Contractors

New rules heighten compliance focus:

- Joint & Several Liability (from April 2026): Agencies and clients may face liability for unpaid PAYE/NICs in umbrella chains, extending scrutiny to international arrangements.

- Making Tax Digital expansion: Higher earners (over £50,000 qualifying income) face mandatory digital records from April 2026.

- IR35 overseas: Primarily applies to UK tax residents; non-residents providing UK services may fall outside if no UK tax charge, but seek specialist advice.

These changes underscore the need for robust payroll partners.

Sector-Specific Challenges in Energy, Engineering, and Construction

Contractors in these fields often face long overseas assignments, local social security equivalents to NICs, visa requirements, and accommodation clauses.

CIS may apply for UK-based construction elements, even abroad. Risks include accidental residency creation or penalties for non-compliance.

Compliant solutions mitigate these by handling deductions, submissions, and benefits seamlessly.

How Futurelink Group Ensures Compliance for Overseas Work

With 30 years of expertise, Futurelink Group offers tailored payroll options for contractors working abroad while maintaining UK ties:

- Sole Trader/Personal Service Company: where status determination concludes that IR35 does not apply, especially with overseas contracting, the self-employed route can be the most efficient way to go.

- Umbrella PAYE: Manages tax/NI deductions, SSP, SMP, pensions, and insurances; ideal for IR35-inside or stability-seeking roles.

- PEO Solutions: Provides full employment status with agency-covered costs, premium benefits, and zero worker deductions beyond standard tax/NI.

- Support Features: Daily payrolls, same-day payments, online portals, tax indemnification, and expert guidance on DTAs and residency.

Clients in energy and construction praise our fast processing and proactive compliance support.

Conclusion

Tax compliance when working overseas in 2026 demands awareness of residency rules, DTAs, and new obligations like Joint & Several Liability to safeguard earnings and avoid penalties. By choosing compliant payroll solutions, contractors in demanding sectors can focus on opportunities while ensuring full adherence. Futurelink Group’s proven services deliver peace of mind through expert handling of cross-border complexities.

Ready to Navigate Overseas Tax Compliance?

Contact Futurelink Group today for personalised advice on umbrella PAYE, PEO, or other solutions tailored to your international assignments. Call +44 (0) 1923 277900 or email sales@futurelinkgroup.co.uk.

Frequently Asked Questions About Tax Compliance Working Overseas

Contractors often have pressing questions on cross-border tax in 2026. Here we address common concerns based on current HMRC guidance and industry trends.

Use HMRC’s Statutory Residence Test; factors include days in the UK (under 183 often non-resident) and ties like family or property. Track accurately to avoid dual residency issues.

DTAs prevent double taxation by allocating rights; claim relief in the UK for foreign taxes paid, especially if assignments exceed host thresholds.

They target umbrella non-compliance in supply chains; international elements may face indirect scrutiny, making compliant UK providers essential.

Yes, especially for maintaining UK compliance; Futurelink handles deductions, benefits, and submissions while supporting DTA claims.

You may still owe UK tax if resident; DTAs and residency status determine final liability, consult experts early.

Craig Moss

Craig Moss is a seasoned professional in the employment and recruitment industries, based in Kings Langley, UK. With over 30 years of experience, including a successful tenure as a central London realtor handling properties up to £3 million, he now leads an exciting management role at Futurelink Group. Specialising in compliant payroll solutions for contract recruitment, Craig helps clients increase margins by up to 30% while navigating complex legislation. His people-focused approach, honed through decades in sales and people management, ensures both recruiters and workers benefit from tax-efficient, compliant solutions. Passionate about building strong relationships, Craig thrives on delivering results that drive business success.